Repo and Securities Lending

Repo and Reverse Repo Rate

Learning Outcome

5

Trace the impact of Repo Rate changes on the economy.

4

Relate rates to loans, EMIs, and savings.

3

Understand their role in monetary policy.

2

Differentiate borrowing, lending, and applicable rates.

1

Define Repo and Reverse Repo.

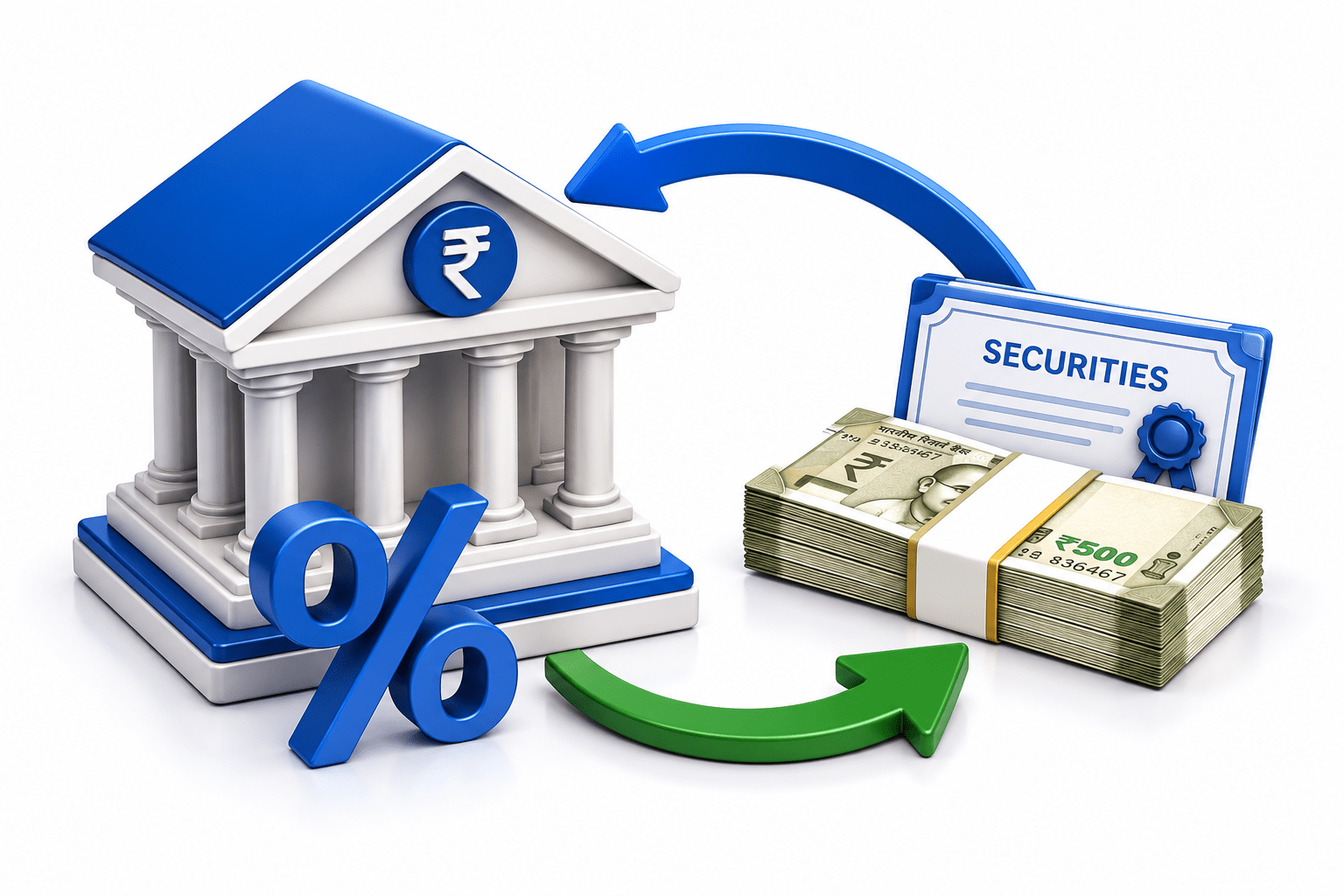

What is Repo Rate?

Repo Rate is the interest rate at which banks borrow funds from the RBI by pledging government securities as collateral.

Real-life link:

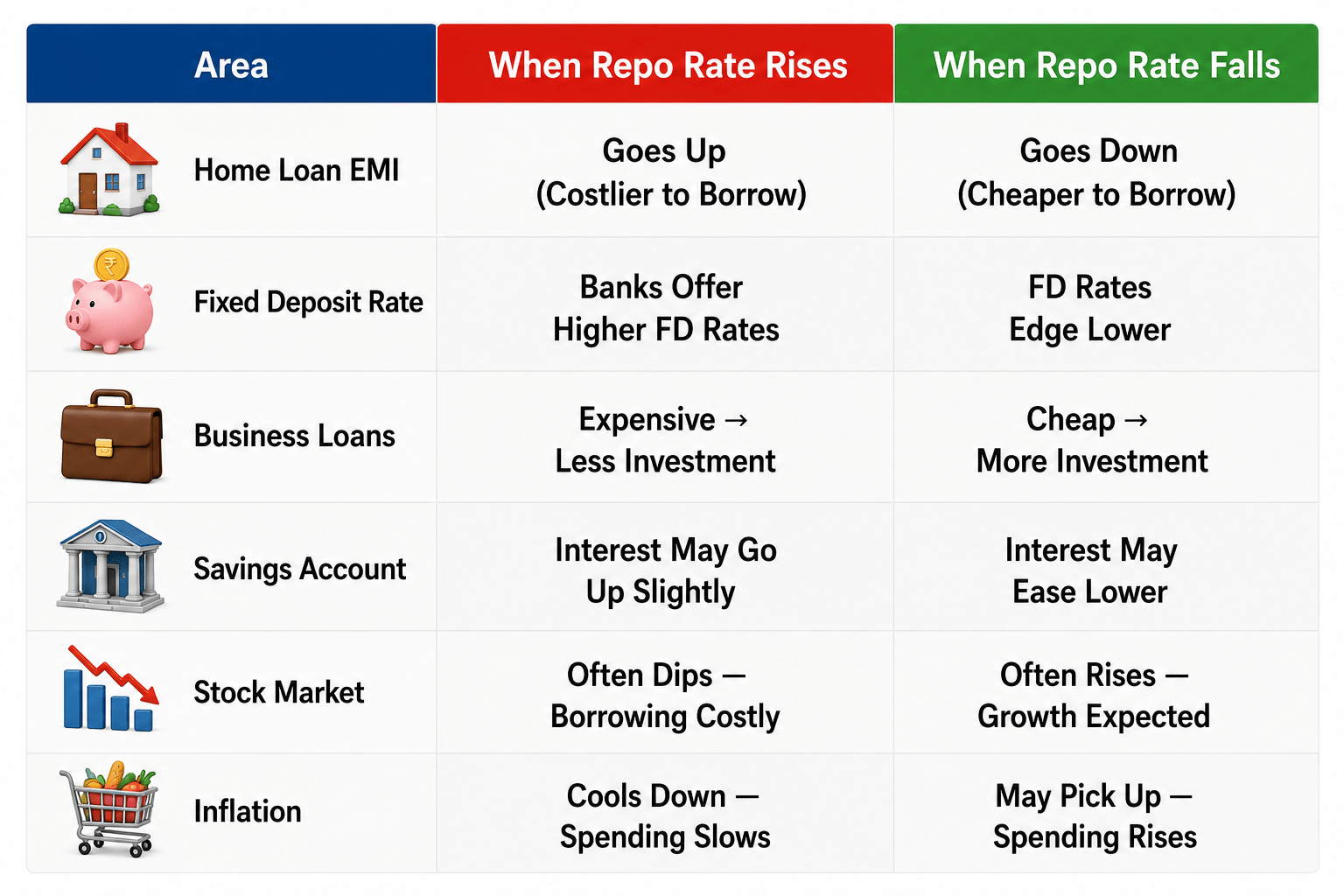

- When RBI raises the Repo Rate, banks pay more to borrow from RBI.

- Banks then charge you more on home loans and car loans.

- When RBI cuts the Repo Rate, your EMI goes down.

|

In short |

Repo Rate = The price banks pay to borrow cash from RBI overnight. Higher rate → Loans get expensive. Lower rate → Loans get cheaper. |

Step-by-Step: How a Repo Works (with Example)

- SBI needs ₹1,000 Crore overnight to meet its daily cash requirements.

- SBI goes to the RBI's LAF (Liquidity Adjustment Facility) window.

- SBI temporarily gives Govt Securities worth ₹1,000 Cr to the RBI.

- RBI gives SBI ₹1,000 Cr cash immediately.

- Next day: SBI returns ₹1,000 Cr + interest (₹14.38 Lakh) at 5.25% Repo Rate.

- RBI returns the Govt Securities to SBI. Deal closed.

Quick Math

Loan Amount: ₹1,000 Crore

Repo Rate: 5.25% per annum

Duration: 1 day (overnight)

Interest = ₹1000 Cr × 5.25% ÷ 365 = ₹14.38 Lakh

SBI pays ₹14.38 Lakh to RBI as borrowing cost.

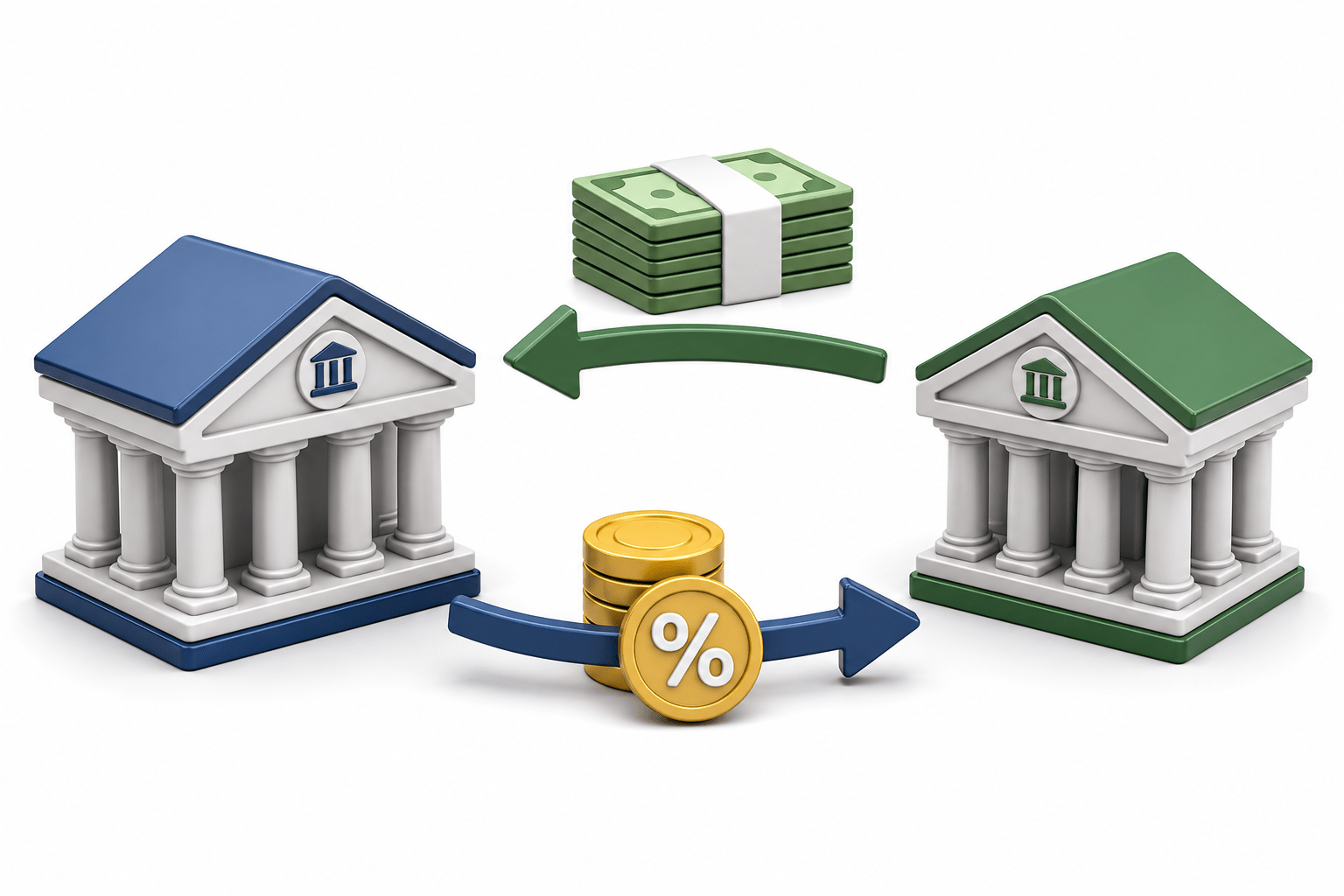

What is Reverse Repo Rate?

Reverse Repo Rate is the interest rate the RBI pays banks for depositing excess funds with it for a short period.

Real-life link:

When RBI raises the Reverse Repo Rate, banks find it more attractive to park money with RBI rather than lend it out.

Less lending → less money circulating → inflation cools down.

In short

Reverse Repo Rate = The return a bank earns when it deposits surplus cash with RBI.

Higher rate → Banks prefer to park money with RBI. Less lending in the market.

Step-by-Step: How a Reverse Repo Works (with Example)

-

HDFC Bank has ₹500 Crore surplus cash at the end of the day — more than it needs.

-

HDFC deposits this ₹500 Cr with the RBI through the Reverse Repo window.

-

RBI gives HDFC Govt Securities as collateral (safety deposit).

-

Next day: RBI returns ₹500 Cr + interest (₹4.59 Lakh) at 3.35% Reverse Repo Rate.

-

HDFC returns the Govt Securities. Deal closed.

-

Zero risk — because the counterparty is the RBI itself.

Quick Math

Deposit Amount: ₹500 Crore

Reverse Repo Rate: 3.35% per annum

Duration: 1 day (overnight)

Interest = ₹500 Cr × 3.35% ÷ 365 = ₹4.59 Lakh

HDFC earns this ₹4.59 Lakh from RBI — completely risk-free.

Real Impact on Banks and Customers

Summary

5

RBI uses both to manage liquidity and inflation.

4

Higher Reverse Repo = More funds parked with RBI.

3

Higher Repo = Costlier loans.

2

Reverse Repo Rate: Rate banks earn from RBI deposits.

1

Repo Rate: Rate at which banks borrow from RBI.

Quiz

Repo Rate is the rate at which:

A. Customers borrow from banks

B. Banks borrow from RBI

C. RBI borrows from banks

D. Companies borrow from banks

Quiz-Answer

Repo Rate is the rate at which:

A. Customers borrow from banks

B. Banks borrow from RBI

C. RBI borrows from banks

D. Companies borrow from banks